I think it is likely that all of you have used an AI agent in some form or other this year. They are great, aren’t they? Even if it is not about saving you time from coding, but simply a shortcut to googling, AI empowers and makes you look ‘smart’. “Look smart”…80% of the time, at best[1]. In some cases, AI will give you the wrong output more than 50% of the time. That’s because large language models (LLMs) operate on data correlations, and are fundamentally probabilistic. It is safe to say that most of the time, AI does not make you money. In some cases (see reference below), businesses actually lose money because of AI.

Ok, you say, but these are early days; at some point, AI will become AGI, and then it will ‘make sense’ and probably make a lot of money. Absolutely, but at what cost, and when? For how long can hyperscalers invest $1Tn per year without raising new capital? How much longer can closed-frontier AI models continue to provide free access and subsidise consumers before investors pull the plug on further fundraising for them? When one excludes circular revenue generation, what is the actual return on AI investments (ROAII)? What is the frontier model’s moat that Open/Chinese AI equivalents cannot cross?

Hyperscalers are already running out of free cash and have resorted to issuing new equities (Alphabet and Oracle) and bonds (Alphabet, Oracle, Meta, Amazon, Microsoft). In fact, combined, the hyperscalers have issued more debt YTD than all of last year. When you add the massive IPOs from SpaceX, Anthropic and OpenAI, and all the other announced IPOs, net equity

issuance (so, net of share buybacks) will probably be the largest we have seen since at least 1999[2]. With no new demand on the horizon (‘everyone’ globally is already very overweight US equities), this heralds a big break in the equilibrium.

In a blast from the past, those hyperscalers are using SPVs and circular accounting to report paper revenues and avoid capital destruction. For example, according to McKinsey[3], global data centres built-out will cost $7Tn by 2030: no amount of free cash flow will be able to cover this unprecedented CAPEX, which means even more debt and equity issuance. But that is not the end of it: with a much shorter depreciation cycle, the rate of CAPEX expansion may slow down but will continue to be substantial thereafter.

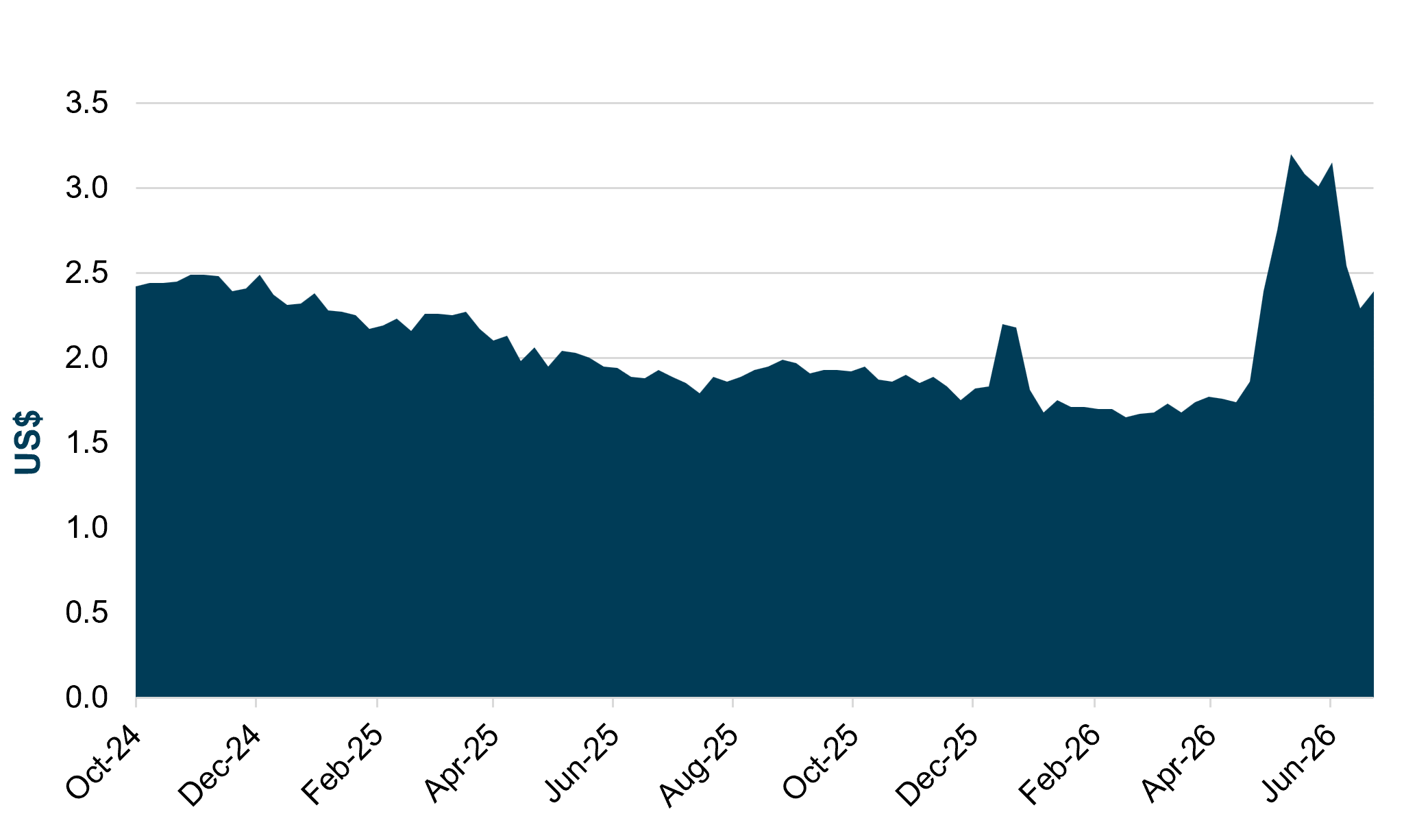

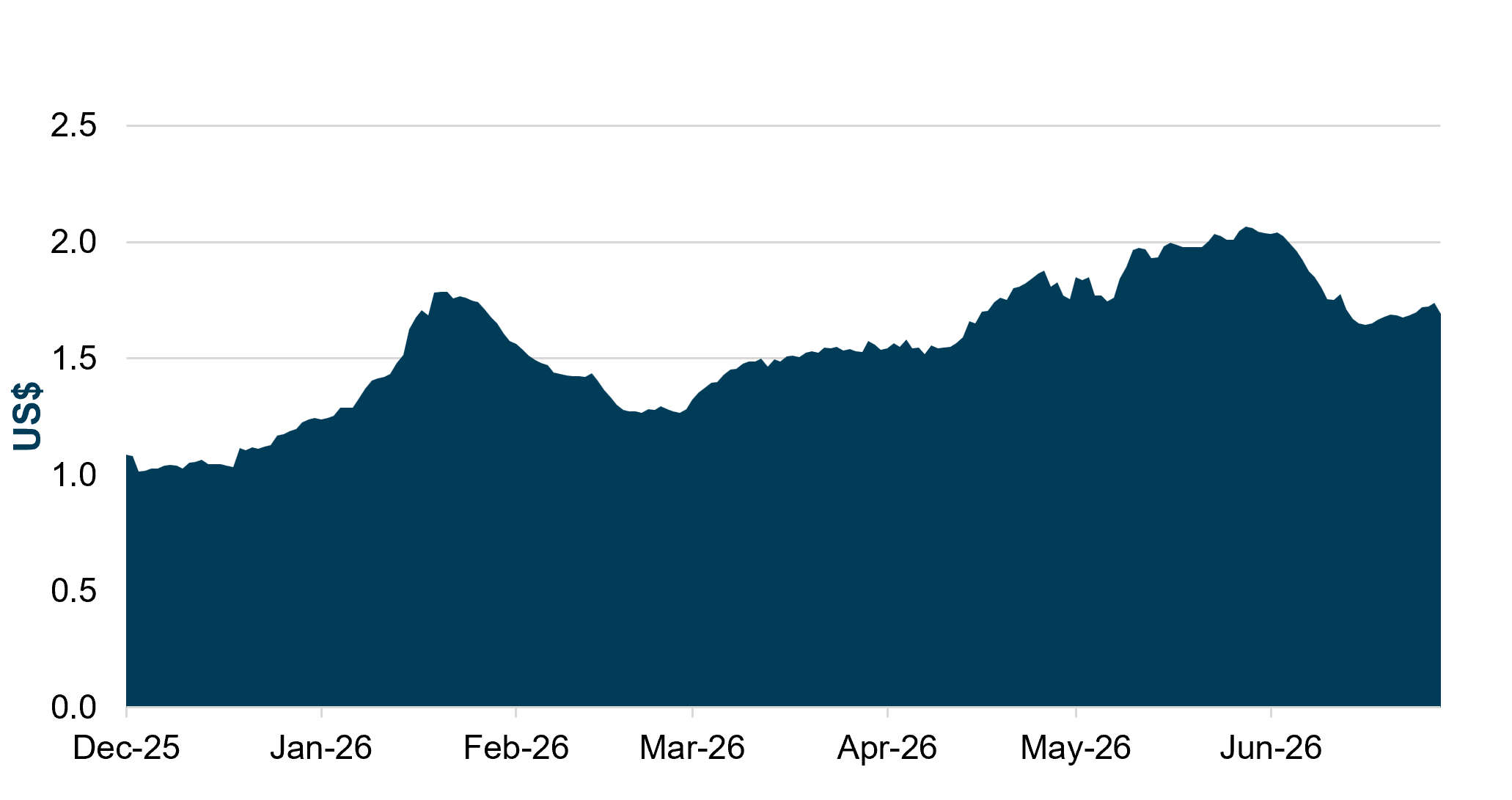

People comparing the internet revolution to the AI one and claiming this time it is different, yes, it is. AI companies are much more about hardware than software, revenue scaling is at a much lower rate, and margins will be much smaller. My view is simply that the hyperscalers will actually start scaling down, not up. Judging by the spot price of Nvidia H100 compute in the on-demand market, that may already have happened.