Now, Iran will never give up strategic control of the Strait. If they allow ships through, it will be on their terms as the Strait is their only guarantee of sovereignty, a potential cash cow tolling booth and a platform to project Iran’s rising military prowess across the region.

The only chance of a peace deal is if Iran deigns to provide Trump with an off-ramp. Iran, after all, certainly doesn’t want another forever war, and if it can come out of this mess with control of the Strait, then this will be a fine strategic victory. There’s a deal there somewhere.

Given Trump’s insistence that the Iran’s ‘two weeks away’ nuclear programme was the stated reason he started the war in the first place, a concession on the nuclear issue is perhaps the most likely compromise that Iran will make to allow Trump to save face.

But as Trump will have to concede the Strait, and therefore by extension, US hegemony in the region (and world), it is unlikely Trump will bite.

Whichever way you game this scenario, it is very hard to see the Strait opening to normal traffic for the foreseeable future. Trump has painted himself into a corner, and he surely knows he is finished politically if he concedes; either destroyed by his “donors” or his MAGA base. It matters not one jot – he is personally all in.

And all the time, massive troop build-ups into the region, suggesting that this is but a brief pause to allow for restocking and another stab at “Epic Fury” (Mk2). The current status quo ceasefire is clearly an unstable equilibrium, as even if Trump extends peace negotiation deadlines indefinitely (his current preferred strategy as it wrests the remaining narrative control away from the Iranians), the clock is ticking in the real world: the physical oil markets.

From a physical oil market perspective, we are entering a new phase where onsite draws should start materialising quite rapidly. Iran has done the hard work, in the sense that it has managed to ‘survive’ while the world’s oil supply buffers, such as SPR releases, sanctions waivers, and oil-on-water drawdowns, are being exhausted.

Over the next week, the last cargoes that left the Strait will have been discharged, so we should expect pump shortages very soon. The higher the oil price, and the worse the shortages are, the more it only serves to increase Iran’s leverage. So until the real shortages bite, Iran won’t be willing to make a deal (even a token uranium inspection) because they’d be leaving a lot of leverage on the table.

And this brings us on to financial markets. The US administration knows that an escalating oil price only favours Iran in this conflict, and so they have countered this with a censorship and misinformation campaign that seeks to significantly downplay the energy infrastructure damage, while magnifying the destruction of Iranian capabilities.

Trump’s tweeting, while on the surface seems increasingly unhinged, is actually quite intentional and very effective. Barack Obama said it best ““You just have to flood a country’s public square with enough raw sewage. You just have to raise enough questions, spread enough dirt, plant enough conspiracy theorizing that citizens no longer know what to believe.”.

Trump is a master at this seditious game, and although Iran is winning the real war, Trump is, almost singlehandedly, winning the information war.

What is so surreal about the current situation is that while any sane person has long ago discounted Trump’s ramblings as pure gaslighting, the ‘market’ is becoming increasingly leveraged to the headlines. Unfortunately, this is by design and is where the core of the deceit lies.

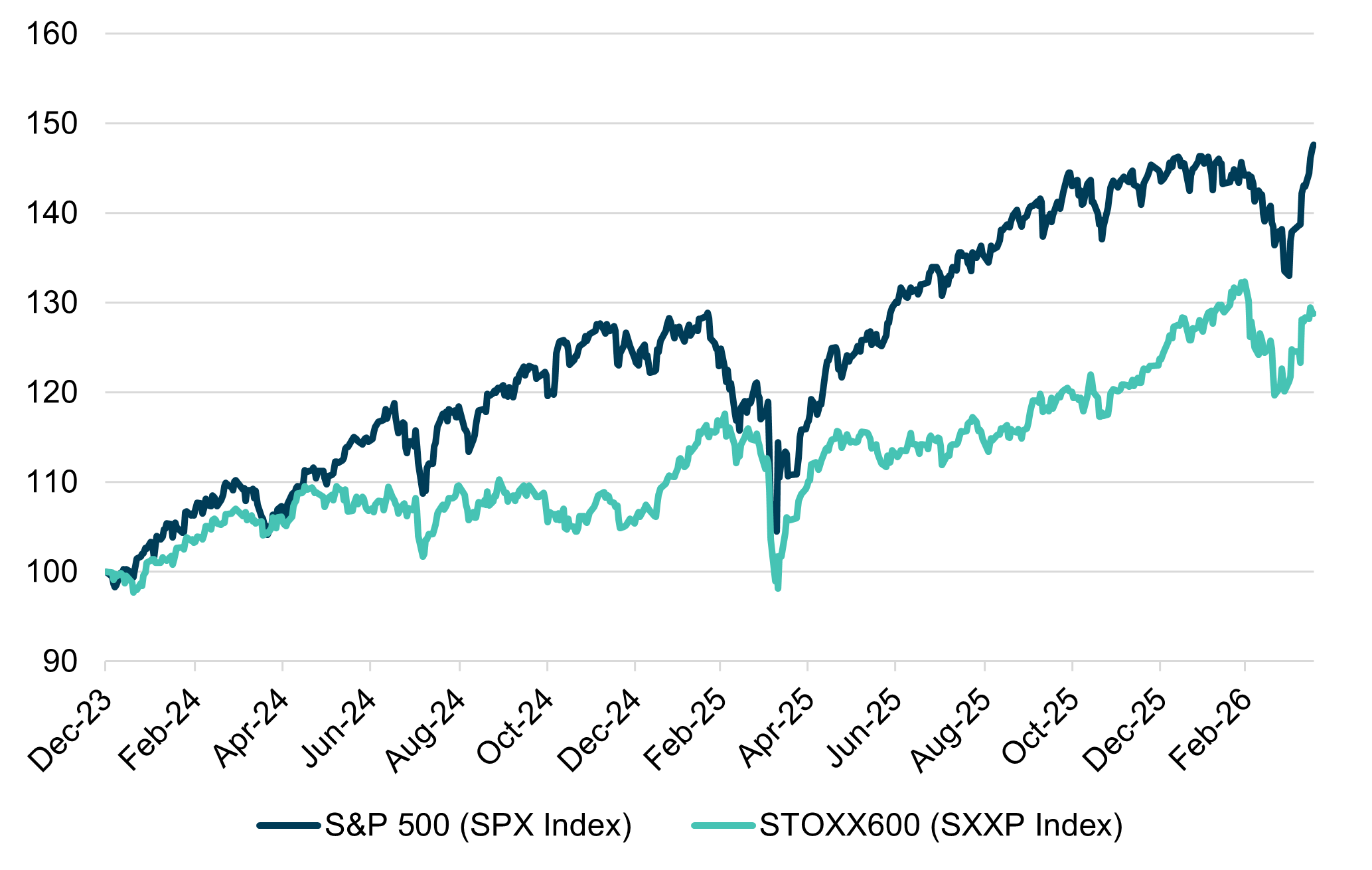

In order to maximise the market impact of the tweets, the US Treasury has reportedly opened brokerage accounts with a well-known quant-trading market-maker to help manage the oil market. Various option-based strategies have been utilised to suppress implied volatility and price levels of oil. The world is watching Brent and WTI. Keep it down, and you’re winning.

Similar suspicious flows, timed around Trump’s tweets, have been observed in VIX futures and zero-day option markets. Again, a possible mixture of frontrunning and swamping the market with bullish flow. Likely, for the sole purpose of profiteering and painting the tape.

Likewise, huge volumes of forced selling of oil futures are pushed through the markets, timed just before and just after the tweets go live. 100 USD on WTI seems to be the level that the administration is defending at all costs. A nice round number, I suppose.

To coincide with the alleged Oil paper price manipulation, central bank printing is working in overdrive behind the scenes in a pre-emptive move to control bond markets and currencies. The potential demise of the petrodollar represents an existential threat to the dollar system and, by extension, US hegemony. Central banks have their work cut out for them.

Keeping markets stable not only panders to Trump’s ego (an unfortunate but absolutely necessary evil), but it is an essential component of US power projection and hegemony, which the war threatens to destabilise. From America’s point of view, the financial markets are an integral part of the overall war strategy. It is their Front line, defended at all costs, in a hyper-financialised system.

To that end, we have seen a huge pickup in dollar swap lines, repo financing of various flavours and the levels of FED purchases of short dated T-bills that are now rivalling the good old days of QE, while the Treasury (not to be out done by), has been busy buying back long dated bonds in record quantities, financed by FED T-bill purchases.